[arellano] get rid of jitclass #131

There are no files selected for viewing

| Original file line number | Diff line number | Diff line change |

|---|---|---|

|

|

@@ -4,7 +4,7 @@ jupytext: | |

| extension: .md | ||

| format_name: myst | ||

| format_version: 0.13 | ||

| jupytext_version: 1.15.2 | ||

| kernelspec: | ||

| display_name: Python 3 (ipykernel) | ||

| language: python | ||

|

|

@@ -77,6 +77,7 @@ import random | |

|

|

||

| import jax | ||

| import jax.numpy as jnp | ||

| from collections import namedtuple | ||

| ``` | ||

|

|

||

| Let's check the GPU we are running | ||

|

|

@@ -365,55 +366,43 @@ The output process is discretized using a [quadrature method due to Tauchen](htt | |

|

|

||

| As we have in other places, we accelerate our code using Numba. | ||

|

|

||

| We define a namedtuple to store parameters, grids and transition | ||

| probabilities. | ||

|

|

||

| ```{code-cell} ipython3 | ||

| Arellano_Economy = namedtuple('Arellano_Economy', ('β', 'γ', 'r', 'ρ', 'η', 'θ', \ | ||

| 'B_size', 'y_size', \ | ||

| 'P', 'B_grid', 'y_grid', 'def_y')) | ||

|

There was a problem hiding this comment. As noted above, we can migrate the comments below to here. (Also, we can change lines without |

||

| ``` | ||

|

|

||

| ```{code-cell} ipython3 | ||

| def create_arellano(B_size=251, # Grid size for bonds | ||

| B_min=-0.45, # Smallest B value | ||

| B_max=0.45, # Largest B value | ||

| y_size=51, # Grid size for income | ||

| β=0.953, # Time discount parameter | ||

| γ=2.0, # Utility parameter | ||

| r=0.017, # Lending rate | ||

| ρ=0.945, # Persistence in the income process | ||

| η=0.025, # Standard deviation of the income process | ||

| θ=0.282, # Prob of re-entering financial markets | ||

| def_y_param=0.969): # Parameter governing income in default | ||

|

There was a problem hiding this comment. I think we prefer to comment on parameters when they are defined for the first time. Please move these comments on parameters to where we define the There was a problem hiding this comment. Thanks @HumphreyYang , I will add the comments to both places, given the comments from another PR. |

||

| # Set up grids | ||

| B_grid = jnp.linspace(B_min, B_max, B_size) | ||

| mc = qe.markov.tauchen(y_size, ρ, η) | ||

| y_grid, P = jnp.exp(mc.state_values), mc.P | ||

|

|

||

| # Put grids on the device | ||

| B_grid = jax.device_put(B_grid) | ||

| y_grid = jax.device_put(y_grid) | ||

| P = jax.device_put(P) | ||

|

|

||

| # Output received while in default, with same shape as y_grid | ||

| def_y = jnp.minimum(def_y_param * jnp.mean(y_grid), y_grid) | ||

|

|

||

| return Arellano_Economy(β=β, γ=γ, r=r, ρ=ρ, η=η, θ=θ, B_size=B_size, \ | ||

| y_size=y_size, P=P, B_grid=B_grid, y_grid=y_grid, \ | ||

| def_y=def_y) | ||

| ``` | ||

|

|

||

| Here is the utility function. | ||

|

|

@@ -473,6 +462,7 @@ def T_d(v_c, v_d, params, sizes, arrays): | |

| β, γ, r, ρ, η, θ = params | ||

| B_size, y_size = sizes | ||

| P, B_grid, y_grid, def_y = arrays | ||

|

|

||

| B0_idx = jnp.searchsorted(B_grid, 1e-10) # Index at which B is near zero | ||

|

|

||

| current_utility = u(def_y, γ) | ||

|

|

@@ -519,7 +509,6 @@ def bellman(v_c, v_d, q, params, sizes, arrays): | |

| # Return new_v_c[i_B, i_y, i_Bp] | ||

| val = jnp.where(c > 0, u(c, γ) + β * continuation_value, -jnp.inf) | ||

| return val | ||

| ``` | ||

|

|

||

| ```{code-cell} ipython3 | ||

|

|

@@ -558,8 +547,8 @@ def update_values_and_prices(v_c, v_d, params, sizes, arrays): | |

| return new_v_c, new_v_d | ||

| ``` | ||

|

|

||

| We can now write a function that will use an instance of `Arellano_Economy` and | ||

| the functions defined above to compute the solution to our model. | ||

|

|

||

| One of the jobs of this function is to take an instance of | ||

| `Arellano_Economy`, which is hard for the JIT compiler to handle, and strip it | ||

|

|

@@ -570,14 +559,16 @@ down to more basic objects, which are then passed out to jitted functions. | |

|

|

||

| def solve(model, tol=1e-8, max_iter=10_000): | ||

| """ | ||

| Given an instance of `Arellano_Economy`, this function computes the optimal | ||

| policy and value functions. | ||

| """ | ||

| # Unpack | ||

|

|

||

| β, γ, r, ρ, η, θ, B_size, y_size, P, B_grid, y_grid, def_y = model | ||

|

|

||

| params = β, γ, r, ρ, η, θ | ||

| sizes = B_size, y_size | ||

| arrays = P, B_grid, y_grid, def_y | ||

|

|

||

| # Initial conditions for v_c and v_d | ||

| v_c = jnp.zeros((B_size, y_size)) | ||

|

|

@@ -605,7 +596,7 @@ Let's try solving the model. | |

| ```{code-cell} ipython3 | ||

| :hide-output: false | ||

|

|

||

| ae = create_arellano() | ||

| ``` | ||

|

|

||

| ```{code-cell} ipython3 | ||

|

|

@@ -637,8 +628,9 @@ def simulate(model, T, v_c, v_d, q, B_star, key): | |

|

|

||

| """ | ||

| # Unpack elements of the model | ||

| B_size, y_size = model.B_size, model.y_size | ||

| B_grid, y_grid, P = model.B_grid, model.y_grid, model.P | ||

|

|

||

| B0_idx = jnp.searchsorted(B_grid, 1e-10) # Index at which B is near zero | ||

|

|

||

| # Set initial conditions | ||

|

|

@@ -695,18 +687,15 @@ def simulate(model, T, v_c, v_d, q, B_star, key): | |

|

|

||

| Let’s start by trying to replicate the results obtained in {cite}`Are08`. | ||

|

|

||

| In what follows, all results are computed using parameter values of `Arellano_Economy` created by `create_arellano`. | ||

|

|

||

| For example, `r=0.017` matches the average quarterly rate on a 5 year US treasury over the period 1983–2001. | ||

|

|

||

| Details on how to compute the figures are reported as solutions to the | ||

| exercises. | ||

|

|

||

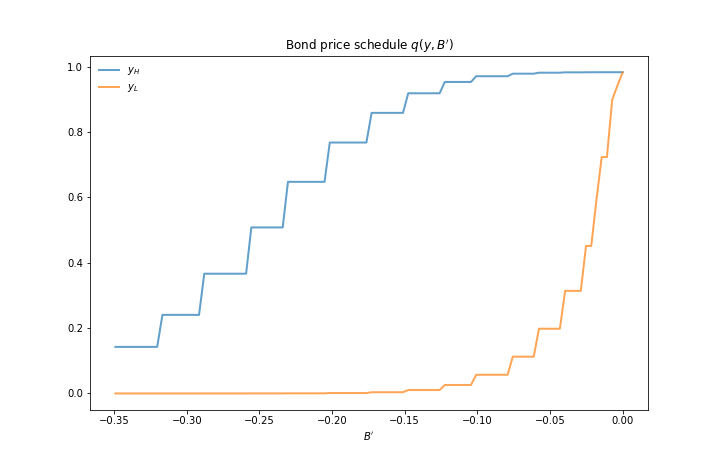

| The first figure shows the bond price schedule and replicates Figure 3 of | ||

| {cite}`Are08`, where $ y_L $ and $ Y_H $ are particular below average and above average | ||

| values of output $ y $. | ||

|

|

||

|  | ||

|

There was a problem hiding this comment. Should we move these images to this repo as we will migrate the advanced series to theme-specific series soon? (CC @mmcky): There was a problem hiding this comment. Thanks @HumphreyYang . I reckon @mmcky have already done that in PR #141 |

||

|

|

@@ -716,7 +705,7 @@ values of output $ y $. | |

| - $ y_H $ is 5% above the mean of the $ y $ grid values | ||

|

|

||

|

|

||

| The grid used to compute this figure was relatively fine (`y_size, B_size = 51, 251`), which explains the minor differences between this and | ||

| Arrelano’s figure. | ||

|

|

||

| The figure shows that | ||

|

|

@@ -766,7 +755,7 @@ Periods of relative stability are followed by sharp spikes in the discount rate | |

|

|

||

| To the extent that you can, replicate the figures shown above | ||

|

|

||

| - Use the parameter values listed as defaults in `Arellano_Economy` created by `create_arellano`. | ||

| - The time series will of course vary depending on the shock draws. | ||

|

|

||

| ```{exercise-end} | ||

|

|

@@ -785,18 +774,18 @@ Compute the value function, policy and equilibrium prices | |

| ```{code-cell} ipython3 | ||

| :hide-output: false | ||

|

|

||

| ae = create_arellano() | ||

| v_c, v_d, q, B_star = solve(ae) | ||

| ``` | ||

|

|

||

| Compute the bond price schedule as seen in figure 3 of {cite}`Are08` | ||

|

|

||

| ```{code-cell} ipython3 | ||

| :hide-output: false | ||

|

|

||

| # Unpack some useful names | ||

| B_grid, y_grid, P = ae.B_grid, ae.y_grid, ae.P | ||

| B_size, y_size = ae.B_size, ae.y_size | ||

| r = ae.r | ||

|

|

||

| # Create "Y High" and "Y Low" values as 5% devs from mean | ||

|

|

@@ -811,7 +800,7 @@ x = [] | |

| q_low = [] | ||

| q_high = [] | ||

| for i, B in enumerate(B_grid): | ||

| if -0.35 <= B <= 0: # To match fig 3 of Arellano (2008) | ||

| x.append(B) | ||

| q_low.append(q[i, iy_low]) | ||

| q_high.append(q[i, iy_high]) | ||

|

|

||

There was a problem hiding this comment.

Choose a reason for hiding this comment

The reason will be displayed to describe this comment to others. Learn more.

Class (

namedtuple) names should follow CamelCaseThere are some

Arellano_Economybelow in the text as well, so please update them together : )There was a problem hiding this comment.

Choose a reason for hiding this comment

The reason will be displayed to describe this comment to others. Learn more.

Good idea! We should change the name in the original lecture too:

https://python-advanced.quantecon.org/arellano.html